Introduction

Overspending quietly undermines financial control and long‑term stability. A lot of men earn steady incomes, yet still struggle to save because daily spending habits go unchecked. Small purchases like coffee, subscriptions, and takeout can slowly drain hundreds of dollars each month without notice. Research found that over 40% of households regularly overspend and later regret those choices, highlighting real patterns of uncontrolled spending.

This research shows that overspending behaviors relate to how people mentally manage money and fail to account for future financial needs. Awareness and structured control of spending are critical. By identifying where money leaks occur and applying disciplined habits, you can stop unnecessary expenses, protect your savings, and build stronger financial strength. In this article, you will learn eight straightforward and practical ways to avoid overspending and take control of your finances, with actionable steps designed to deliver measurable improvements over time.

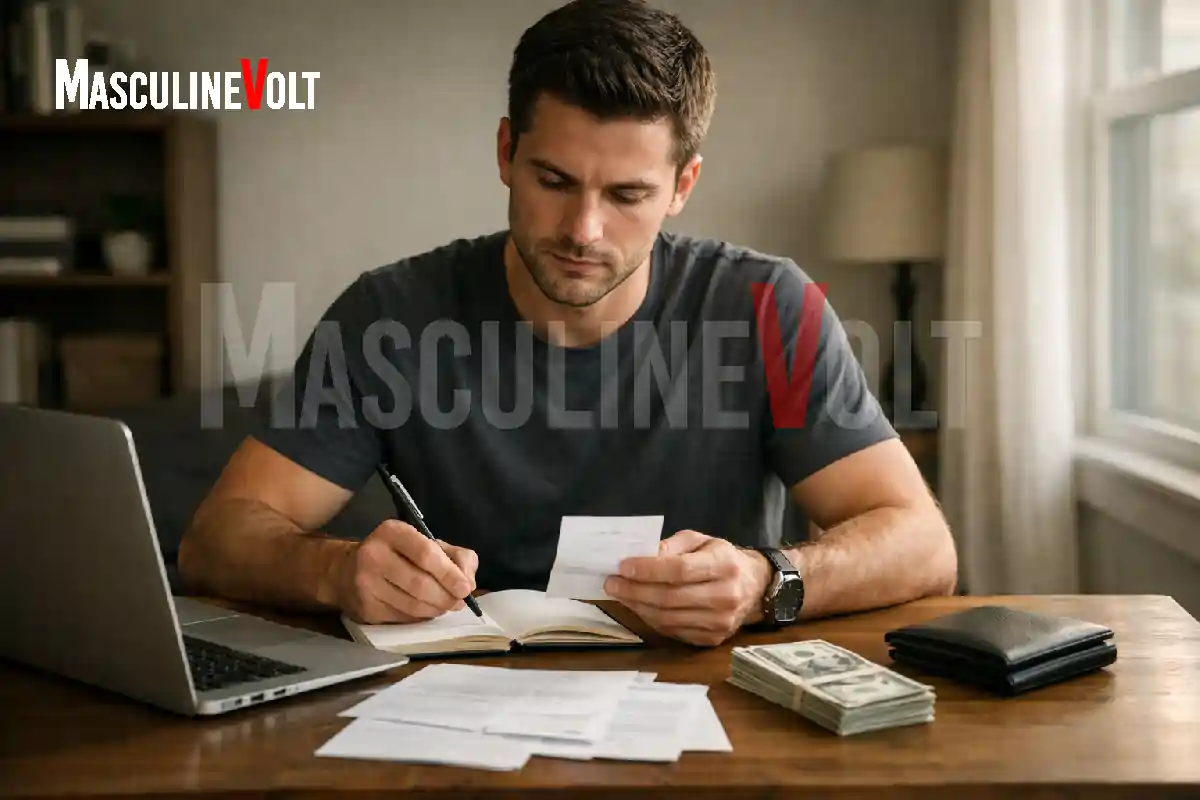

1. Track Every Single Expense

A lot of people spend without realizing how small purchases add up. Daily items such as coffee, snacks, ride-sharing, online subscriptions, and convenience foods can quietly consume hundreds of dollars each month. Begin by writing down every expense immediately.

Use a notebook, spreadsheet, or budgeting app to make this process consistent. Over time, patterns will appear. You may notice that lunch deliveries cost $150 a month or subscriptions take $80 from your income. When you see the totals, you can make deliberate decisions to reduce or remove unnecessary spending. Tracking also builds accountability. You cannot improve what you do not measure. According to research, expense tracking acts as a form of self-regulation that improves spending control and reduces impulsive financial behavior over time.

Daily tracking also prevents impulse spending because each purchase must be noted. You can also set reminders to log expenses at the end of the day. Consistent tracking increases awareness, strengthens discipline, and ensures that your income is directed toward priorities such as savings, investments, or debt repayment. Over time, this habit transforms your spending into a controlled and purposeful system.

2. Create a Monthly Spending Plan

A lot of men spend first and regret later because income is not allocated. Start by categorizing your money into housing, food, transportation, savings, investments, and discretionary spending. Assign a specific amount to each category based on your income and priorities. For example, if your monthly income is $3,000, you might allocate $900 to housing, $300 to food, $200 to transportation, $500 to savings, and $600 to other essentials and discretionary items. This method ensures that money is used intentionally and prevents overspending on non-essential items.

Monthly plans also allow you to adjust categories when needed. If you spend less on transportation one month, you can move the extra funds to savings or debt repayment. Reviewing the plan at the end of each month helps identify weaknesses and improve allocation. Purposeful planning removes surprises and makes financial goals achievable. Structured budgeting also creates confidence. You always know where your money goes. Over time, a monthly spending plan establishes consistency, improves financial control, and ensures that your money works for you rather than disappearing without notice. Smart planning turns income into a tool for growth instead of a source of stress.

3. Delay Purchases for 24 Hours

Do not feel pressure to buy items immediately, because marketing creates urgency. Non-essential purchases trigger emotional reactions that fade over time. To counter this, delay any non-critical purchase for twenty-four hours. Use this time to assess whether the item solves a real problem or aligns with your financial goals. For example, you may want a new gadget because it looks appealing, but after one day of reflection, you may realize it is unnecessary.

Delaying purchases reduces impulse buying and allows you to make logical decisions. Over time, this habit strengthens self-discipline and improves savings. You also learn to differentiate between needs and wants. Combining this strategy with expense tracking helps you notice patterns in impulsive spending.

Gradually, unnecessary expenses decline, and money that would have disappeared is redirected toward meaningful goals, such as building an emergency fund or paying down debt. Delaying purchases also prevents regret. Decisions become intentional rather than emotional. Over weeks and months, you gain confidence in controlling your spending and experience less financial stress. Applying this simple method consistently allows you to maintain long-term stability and develop disciplined money habits that compound over time.

4. Avoid Shopping Without a List

The truth nobody will tell you is that, retailers design store layouts and online recommendations to trigger impulse purchases. Men who enter stores without a clear plan are more likely to buy unnecessary items. To prevent this, prepare a specific shopping list before leaving home. Include only essential items such as groceries, toiletries, or work-related purchases. Stick strictly to the list while shopping.

When you follow a list, spending becomes intentional, based on real needs, not emotions or trends. Review the list before checkout and remove items that are not required. This step reinforces discipline. For example, you may add a premium snack to your cart but realize it does not fit your budget and remove it. Over time, controlled shopping improves awareness, reduces waste, and strengthens financial habits. You also spend less time shopping because you focus on essentials.

This approach prevents small purchases from accumulating into significant monthly costs. Intentional shopping combined with tracking and budgeting ensures your money flows toward priorities like savings and investments. Ultimately, using a list is a simple yet highly effective method to maintain financial control and avoid the distractions that lead to overspending.

5. Limit Access to Easy Credit

People with bad spending habits often use credit cards or buy-now-pay-later options for items they cannot afford with cash. The initial payments appear manageable, creating a false sense of financial security. Over time, interest accrues, and balances grow, reducing money available for savings or investments. To maintain control, reduce access to unnecessary credit. Use debit cards or cash for daily purchases to stay aware of spending limits.

For example, paying for coffee, subscriptions, or dining with cash immediately shows the actual cost of each purchase. Limiting credit access prevents hidden interest charges and enforces discipline. Research shows that consumers tend to spend more when using credit cards than cash because credit card payments reduce the psychological “pain of payment,” which increases willingness to spend. Controlled use of credit ensures that borrowing serves long-term goals, such as business investment or property purchase, rather than funding a lifestyle. You remain the owner of your money instead of an obligated debtor. Over time, restricted access to credit reduces financial stress, prevents overspending traps, and strengthens long-term stability.

6. Set Clear Savings Goals

Always have specific targets, so you do not treat saving as optional, leading to inconsistent results. Define an exact amount to save each month and a clear deadline. For example, aim to save $200 each month to create a $2,400 emergency fund within a year. This approach gives each deposit a purpose. Visualize the benefits of your savings, such as financial freedom, security, or investment potential.

Focus on these outcomes to strengthen motivation. Use automatic transfers to ensure consistency. For example, set your bank to transfer money to savings the day after income arrives. Track progress regularly to maintain accountability. Clear goals also reduce temptation because every spending decision considers its impact on your objectives. Over time, structured saving becomes a habit, and financial independence increases. Men who follow targeted savings plans experience less stress, stronger confidence, and better long-term wealth accumulation. Saving intentionally ensures that your money works for you and not for temporary impulses.

7. Reduce Exposure to Social Media Triggers

Social media often encourages overspending, by showcasing luxury lifestyles and instant gratification. Men exposed to such content feel pressure to keep up. Constant comparison drives unnecessary purchases. Limiting exposure reduces temptation and allows focus on personal goals. Unfollow accounts that promote materialism or impulsive buying. Replace scrolling with productive activities such as learning skills or planning finances.

For example, seeing a promoted product may trigger an unplanned purchase, but avoiding the feed prevents this influence. According to research, social media intensity indirectly affects consumer spending behavior through increased materialism, including impulse buying and credit overuse tendencies.

By controlling media consumption, you reinforce discipline and reduce emotional triggers that lead to overspending. Over time, you make deliberate choices, and money flows toward meaningful objectives. Reducing exposure also improves mental focus and supports long-term financial stability.

8. Review Finances Weekly

Regular review of finances will save you from making small mistakes, that will result to becoming large problems. Men who check spending, income, and savings weekly maintain control over their money. Start by reviewing transactions and categorizing expenses. Compare actual spending against your budget. Identify areas that exceed limits and adjust immediately. For example, if dining out costs $200 while the budget allows $150, reduce the next week’s discretionary spending to compensate.

Weekly reviews also provide motivation when progress is visible. Tracking changes reinforces habits and accountability. Over time, weekly financial reviews help detect overspending patterns, prevent debt accumulation, and support long-term goals. Consistency ensures that your finances are aligned with objectives, savings remain on track, and investments grow steadily. This simple habit strengthens discipline and maintains financial authority over time.

In conclusion, overspending quietly undermines financial power. Tracking expenses, planning monthly spending, delaying purchases, shopping with lists, limiting credit, setting savings goals, reducing social media influence, and reviewing finances weekly all strengthen control over money. Discipline, not income alone, builds lasting wealth. Applying these eight strategies consistently ensures that your money supports your goals rather than disappearing. Controlled spending improves confidence, reduces stress, and creates long-term stability. Start implementing these methods today to protect your finances and develop habits that secure wealth for the future.

Finance Related:

Important Financial Decision Every Man Should Take Before 30